Syllabus changes in Cambridge International AS & A Level Business (9609)

There are a number of new areas of study and a considerable amount of material has been switched between AS and A Level. One particularly significant change is that strategy is part of each of the functional areas at A Level and not just a stand-alone section.

Some Changes includes:

1.1.2 Intrapreneurs has been introduced as a topic alongside entrepreneurs

1.3.3 Business growth contains some new material and has been moved to the AS syllabus

3.1.7 Customer relationship marketing has been added

2.1.1 The purpose and roles of human resource management (HRM) has been introduced

5.4 All material on costs is in the AS syllabus and some new material on break-even analysis

6.2 Scenario planning and blue ocean strategy have been added

7.3 A number of new theories of leadership have been introduced and all material on this topic has been

moved to A Level

Topics in the current syllabus which will be no longer covered include:

The marketing mix: the role of the customer (the 4Cs) and using the internet for the 4Ps/4Cs

Sources of finance: short and long-term finance

Cash flow: the construction of cash flow forecasts

Investment appraisal: the internal rate of return (IRR)

Strategic management: Chandler’s assertion and strategy and competitive advantage

Syllabus changes in Cambridge International AS & A Level Economics (9708)

The revised syllabus is now organised into the following six main sections:

1. Basic economic ideas and resource allocation

2. The price system and the micro economy

3. Government microeconomic intervention

4. The macro economy

5. Government macroeconomic intervention

6. International economic issues

Teachers are advised to build learners’ knowledge around the updated seven (rather than the old five) key concepts:

1. Scarcity and choice

2. The margin and decision-making

3. Equilibrium and disequilibrium

4. Time

5. Efficiency and inefficiency

6. Regulation, equality and equity

7. Progress and development

As you would expect, our new edition of Cambridge International AS & A Level Economics has been updated to reflect the changes in the syllabus coverage and structure.

New areas of study include the following:

1.2.1 Economics as a social science

1.3.2 Difference between human capital and physical capital

1.5.4 Significance of a position within a PPC

2.4.3 Relationships between different markets: derived demand

2.4.4 Functions of price in resource allocation: incentivization

2.5.4 Significance of price elasticity of demand and of supply in determining the extent of the changes in consumer and producer surplus

3.1 Reasons for government interventions in markets

3.2.5 Buffer stock schemes

3.2.6 Provision of information

5.1 Government macroeconomic policy objectives

5.2.5 Government spending: types of spending: capital (investment) and current

7.8.4 Other pricing policies: predatory pricing

8.1.1 Application and effectiveness of measures to tackle different forms of market failure: production quota

8.2.5 Policies towards equity and equality, for example: universal basic income

9.2.5 Inclusive economic growth

9.3.3 Voluntary and involuntary unemployment

9.3.6 Mobility of labour

11.6.1 Meaning of globalization and its causes and consequences

Changes to the AS/A Level allocation of topics to balance the content between the two levels include the following:

Topics moved from A Level to AS Level:

3.3 Addressing income and wealth inequality

4.1 National income statistics

4.2 Introduction to the circular flow of income

4.4 Economic growth

4.5 Unemployment

Topics moved from AS Level to A Level:

8.1.1 Application and effectiveness of measures to tackle different forms of market failure: specific and ‘ad valorem’ indirect taxes; nationalization and privatization

9.4.1 Definition, functions and characteristics of money

11.2.1 Measurement of exchange rates: distinction between nominal and real exchange rates · trade-weighted exchange rates

11.2.2 Determination of exchange rates under fixed and managed systems

11.2.3 Distinction between revaluation and devaluation of a fixed exchange rate

11.2.5 The effects of changing exchange rates on the external economy using Marshall-Lerner and J curve analysis

11.6.2 Distinction between a free trade area, a customs union, a monetary union and full economic union

11.6.3 Trade creation and trade diversion

Topics in the current syllabus which will no longer be covered include:

- The Canons of Taxation

- Aggregate Expenditure (AE) function

- Keynesian and Monetarist schools

- The impact of corruption, and importance of the legal framework in an economy

The assessment objectives have been revised into three categories and their weighting in the overall assessment grid has been updated:

AO1: Knowledge and understanding (application is now tested within this objective)

AO2: Analysis

AO3: Evaluation

The weighting of the assessment components in the AS and the overall A Level has been amended to reflect the changes in structure and total marks

Paper 2 now carries 60 marks and its duration is 2 hours

Paper 4 now carries 40 marks and its duration is 2 hours

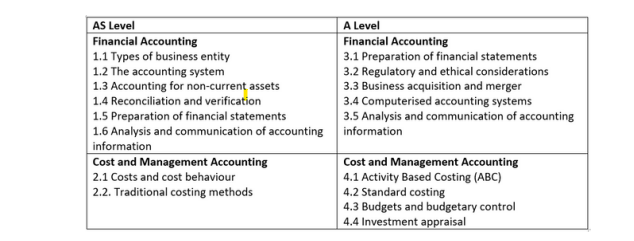

Syllabus changes in Cambridge International AS & A Level Accounting (9706)

The revised syllabus is now organised into the following four main sections:

As you would expect, our new edition of Cambridge International AS & A Level Accounting will be updated to reflect the changes in syllabus coverage and structure. New areas of study include the following:

1.1.1 Types of business entity

1.6.2 Measures to improve the profitability, liquidity and efficiency of an organisation

2.1 The principles of just in time (JIT) management of inventory

2.2.3 Make-or-buy, special orders, closure of business unit and target profit

3.1.3 Clubs and societies (currently on the existing syllabus as ‘not-for-profit’ organisations)

3.1.2 How to evaluate business decisions based on possible changes in the composition of a partnership

3.2.2 Ethical considerations

3.5.1 Interest cover ratio

Topics in the current syllabus which will no longer be covered include:

Folio references

Authorized share capital (as a contrast to issued share capital)

Income gearing ratio

Consignment and joint venture accounts

Sensitivity analysis

Calculation of labor costs using different methods of remuneration including bonus schemes

LIFO as a method of inventory valuation

Preparation of break-even charts

In addition to changes in the topics covered throughout the syllabus, there have also been some adjustments to the delivery of topics between AS & A Level.

Moved from AS Level to A Level:

1.4.3 Partnerships

Prepare capital and current accounts to record changes required in respect of goodwill and revaluation of assets on the

introduction of a new partner, retirement of an existing partner and the dissolution of a partnership.

⤷ Now moved to 3.1.2

2.3 The application of accounting to business planning

The benefit to business planning by the use of accounting data.

Candidates should be able to:

• Explain the need for a business to plan for the future

• Explain why organisations prepare budgets and the benefits they bring to the planning process

• Explain the advantages and disadvantages of budgetary control, including both financial and non-financial factors

⤷ Budgeting is now contained within 4.3

Moved from A Level to AS Level:

1.4 Computerised accounting systems

The need for and the ability to discuss the process of computerising the accounts of a business.

Candidates should be able to:

• Discuss the advantages and disadvantages of introducing a computerised accounting system

• Discuss the process of computerising the business accounts

⤷ Now moved to 1.2.1

In terms of the assessment, there are four externally assessed exam papers.

Paper 1 and Paper 2 assess the AS Level content. Papers 1, 2, 3 and 4 assess the A Level (i.e. the total) content

Paper 1 ‘Multiple choice’ is a 1 hour paper consisting of 30 multiple choice questions based on sections 1 and 2 of the

syllabus content. It counts for 28% of the AS level (or 14% of the A Level)

Paper 2 ‘Fundamentals of accounting’ is a 1 hour 45 minute paper consisting of 4 structured questions based on

sections 1 and 2 of the syllabus. It counts for 72% of the AS level (or 36% of the A Level)

Paper 3 ‘Financial accounting’ is a 1 hour 30 minute paper consisting of 3 structured questions based on section 3 of the syllabus content. It counts for 30% of the A Level

Paper 4 ‘Cost and management accounting’ is a 1 hour paper consisting of 2 structured questions –

based on section 4 of the syllabus. It counts for 20% of the A Level

⤷ For Papers 3 and 4, knowledge of the AS Level content is assumed